Key changes

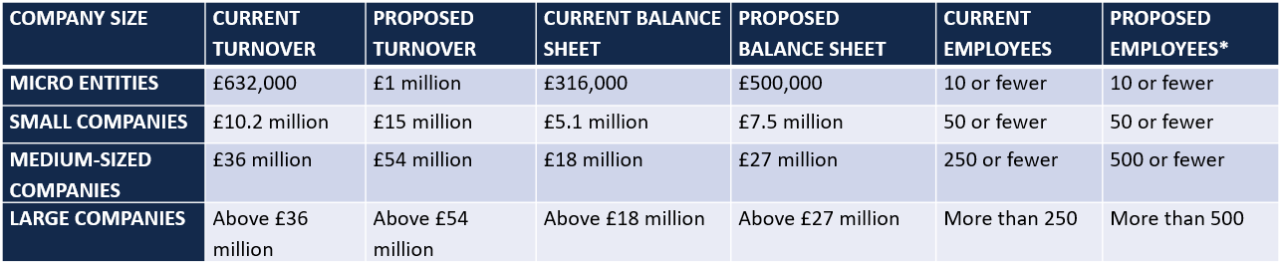

The following table provides a detailed comparison of the current and proposed thresholds for company size classification, with the financial measures being proposed to increase by 50% over the current limits:

* Proposed employee numbers are subject to a future consultation later in 2024

As is currently the case, in order to satisfy the criteria to be a certain size, two out of the three above thresholds must be met in two consecutive years. In addition, a company will not qualify as a micro-entity, small or medium-sized company if it is ineligible or is part of an ineligible group, which includes publicly listed entities, or a business that undertakes insurance market activity.

Further changes which could be enacted include:

The removal of the requirement to present certain non-financial disclosures and strategic reports for medium-sized entities;

The removal of the option to file filleted accounts for small and micro-sized entities, as this proposal was included in the Economic Crime and Corporate Transparency Act which was passed into law in October 2023.

Implementation Timeline

The new thresholds are anticipated to be applicable for financial years starting on or after 1 October 2024.

What are the potential benefits for businesses?

The proposed increase in company size thresholds is a strategic move designed to remove much of the red-tape surrounding the UK’s business environment. Here are some of the key benefits that businesses can expect:

Simplified reporting requirements, especially for those companies that fall into the smaller company threshold limits. This will reduce the administrative time for those businesses to comply with their statutory requirements

Financial savings arising from the reduced administrative burden, and potential savings from lesser audit requirements, especially those that then fall to be exempt from mandatory statutory audits

A greater focus on core activities, with resources that had been previously tied-up with compliance and administrative tasks being redeployed to the core activities of the business

Need assistance

Should you wish to discuss the proposed changes to the company size threshold regime, and how this may impact your business, call 0845 555 8844 or simply complete our enquiry form.