Before businesses apply for loan support under the government backed Coronavirus Business Interruption Loan Scheme (CBILS) perhaps it is worth a few minutes of reflection to consider how to make the application successful?

What do the lenders want?

Lenders will want to properly understand the activities of the business and also the key risks the business faces in the future. Given an appropriate structure they will want to confirm that the borrower can afford to repay any loan finance and that they have sufficient ‘skin in the game’. A funder can only achieve this with a basic narrative which explains the assumptions underpinning the future business plan.

Lenders will also want to assess whether the purpose and amounts are reasonable and that in the event of a problem there is a second source of repayment - this is typically the role of bank security and in the case of CBILS comes in the form of an 80% guarantee from the government.

It is vital that management has assessed risk in the short, medium and long-term. This risk assessment says a lot about the quality of the management team and builds confidence in the plan.

The financial presentation should be clear and unambiguous and should demonstrate what steps (other than raising finance) the business is taking to enhance its ability to repay debt.

In the event that the business has a track record of repaying similar amounts of money or contributing to capital projects with its own cash, a lender will take confidence from this.

Viability

The problem with viability is that it is not clearly defined and as a result it can be difficult to know what lenders really mean when they seek viable propositions.

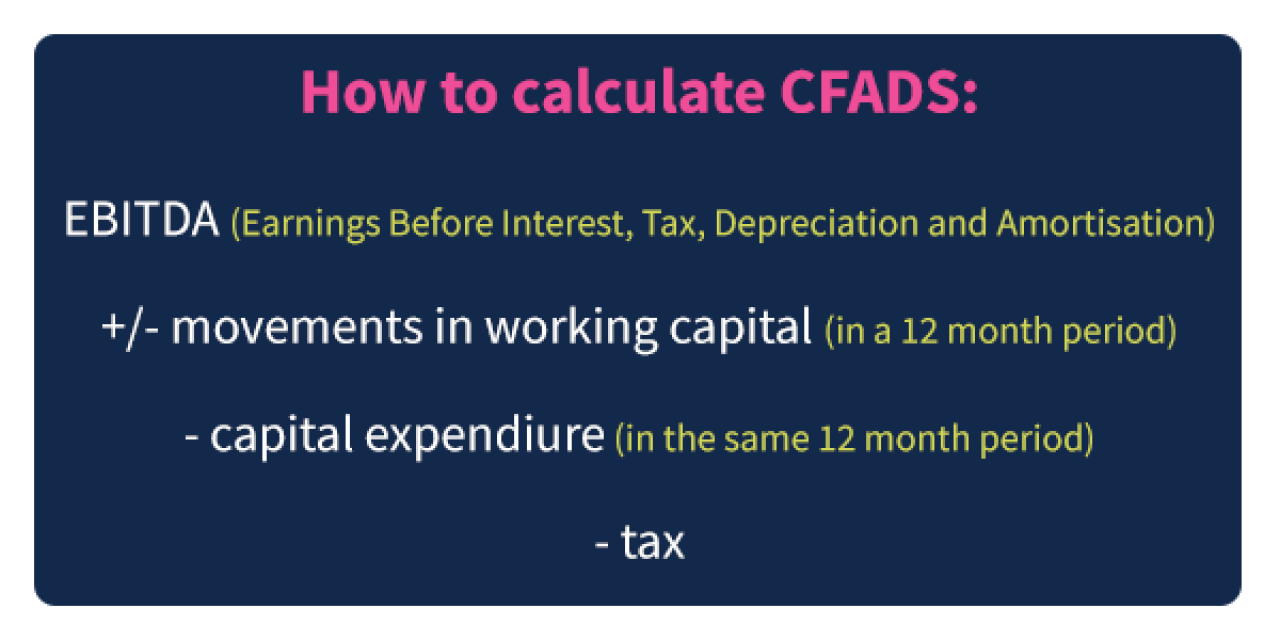

In my opinion, it is essential that businesses can demonstrate serviceability of future loan commitments (the debt service costs) by assessing the Cash Flow Available for Debt Servicing (‘CFADS’) from which it can repay its debt. CFADS can be calculated as follows:

When CFADS is calculated, simply compare CFADS to Total Debt Service Costs (including both capital and interest payments) and assuming there is a comfortable level of headroom after taking into account debt service costs, the financial model is proven. Business should target at least 125% CFADS cover to Total Debt Service Costs but please take advice from lenders, as criteria varies. Some lenders will be happy with as low as 110% cover.

It goes without saying that the model must hold water in terms of the underlying assumptions but proving that the debt is serviceable in the future is a sensible way of building your case.

Consider the ‘What ifs’

Given the current level of uncertainty due to the COVID-19 crisis, it is prudent to plan for an extended period of slower trading. It seems appropriate that forecasts could contain two or three months without significant revenue generation, followed by a build-up of revenue over the following quarter. It is equally appropriate to forecast the benefits of implementing the Coronavirus Job Retention Scheme, which will include staff being furloughed for a period of time.

On the basis that many economists are predicting some form of economic slow-down leading to a recession, it would also be prudent to forecast assuming that invoices may be settled slower than has historically been the case and that some of your customers may not be in business.

Capital intensive businesses should also plan for a level of unplanned capital expenditure in order to perform the most robust sensitivity analysis.

It is appropriate for business owners to sensitise the projections based on their own assessment of risk as opposed to a blanket reduction in turnover which may be somewhat meaningless.

Think about the medium and long term

Although in crisis we are obliged to deal with the here and now, it is vital that businesses consider the medium and long term position.

Lenders are likely to set financial covenants and monitor the business based on projections and there is little point in disguising future events if they are critical to the long term success of the business.

That is not to say the application today should include funding requirements for two to three years’ time but it would be appropriate to share the long term plan with lenders, in order that they can build an understanding of the business and consider the most appropriate financial structure to support the business in the short, medium and long term.

What happens if the model doesn’t work?

In my opinion testing the business plan to destruction is no bad thing and it will help management to decide upon their priorities and to agree the most appropriate financial structure for the business.

Depending upon the plans for the business, all business owners should recognise that asset-based lending, term debt and overdraft borrowing may not be the optimum solution. In the event that the model doesn't work then business owners should take time to consider whether it is wise to take on extra indebtedness or whether the solutions lie elsewhere.

For example, if the business cannot recover from its current financial predicament then it may be necessary to seek advice from a reputable insolvency practitioner. Alternatively, it may simply be the case that equity funding is a much more appropriate method of supporting the business out of the current crisis and through a period of growth.

Funding options

There are a myriad of funders out in the marketplace and hungry to lend money to good quality businesses with a sustainable future.

Businesses are naturally attracted to the government-backed CBILS, not least because the government will provide a guarantee of 80% to the lender and facilities are provided interest and fee free for the first 12 months.

In addition to (over 40) lenders who are able to provide CBILS facilities, there are hundreds of asset-based lenders, peer-to-peer providers, family offices and equity providers as well as regional assistance with schemes such as the Midlands Engine Investment Fund.

Given the breadth of choice it is difficult for business owners to establish the most appropriate funding partner themselves and I recommend speaking to ourselves or one of the many corporate finance and debt advisory teams in the Midlands. Help is out there so please use it.

Take Action Now

To find out more about how Dains can support your business with an application for a Coronavirus Business Interruption Loan, please call 0845 555 8844 or simply complete our enquiry form. Don’t wait, take advice now, we are here to help you.